Old Age Security: Bigger, Smaller, or Better Targeted?

OAS is no longer just a quiet background benefit

In 2022, I wrote about the mechanics of Old Age Security (OAS): who qualifies, how much it pays, how the recovery tax works, and why the Guaranteed Income Supplement matters. This post is different. The mechanics still matter, but the more interesting question today is not simply how OAS works. It is what OAS is supposed to do.

OAS is paid from general federal revenues, not from a dedicated contribution fund like CPP. As Canada ages, the cost of OAS rises. At the same time, the recovery tax (aka the “clawback”) begins at a relatively high level, which means many retirees who are not in obvious financial need still receive full or partial OAS. For couples, the point is even more noticeable because the recovery tax is based on individual income, not household income.

I recall hearing an interesting discussion on Peter Mansbridge’s podcast, The Bridge, in which listeners were asked what federal spending might be reduced. What surprised me was that OAS came up more often than I would have expected, including suggestions that the recovery tax begin at a lower income level. I would not treat that as polling data, but it did strike me as a sign that OAS reform is no longer only a topic for policy analysts.

The issue is not that simple

Seniors are not a single financial category. Some are very comfortable. Others live close to the edge. Many are renters. Many are single, widowed, or without significant workplace pensions. Seniors are constrained by a fixed income, even though they face the same rising costs as everyone else. Groceries, rent, property taxes, utilities, transportation, insurance, and health-related costs do not politely stop rising when someone turns 65. Often, retired seniors cannot easily return to work to make up for these shortfalls.

The Bloc Québécois proposal presses on one side of the problem. If seniors aged 75 and older receive a 10% OAS increase, why not seniors aged 65 to 74? A 68-year-old renter with limited income is not obviously better off than a 75-year-old homeowner with a good pension.

Generation Squeeze presses on another side. It argues that public dollars should not flow so generously to higher-income retirees when lower-income seniors still struggle, and younger Canadians face serious affordability pressures.

The Canadian Centre for Policy Alternatives presses on yet another side. Its general approach is to treat OAS and GIS as part of Canada’s public pension floor, especially for low-income seniors. From that perspective, the priority is less to reduce OAS or GIS spending and more to strengthen income security for seniors at risk of poverty.

These are not simply different answers. They are different ways of defining the problem.

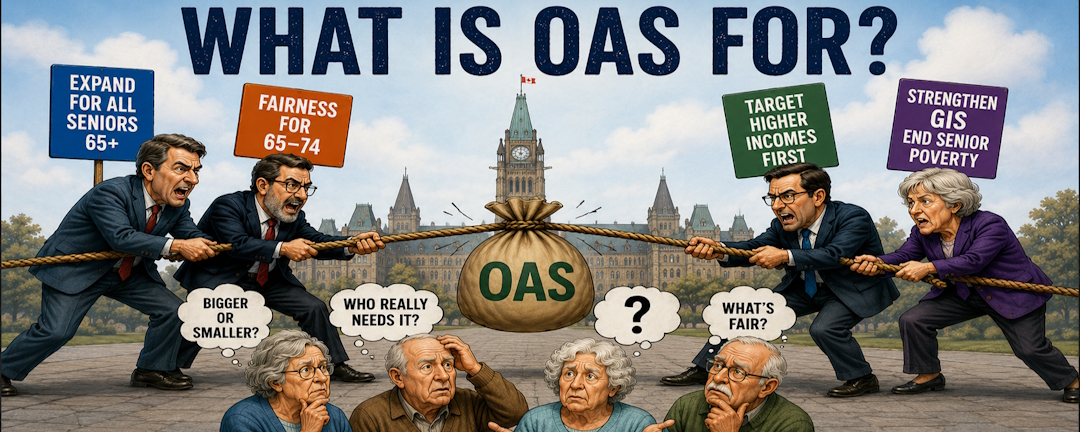

The real question is, “What is OAS for?”

The better question may not be whether OAS should be bigger or smaller. The better question is: What is OAS for?

Is OAS a broad age-based benefit for older Canadians? Is it an anti-poverty program? Is it a supplement to private retirement savings? Is it a recognition of long-term residence in Canada? Is it a politically durable foundation underneath the rest of the retirement income system?

The somewhat awkward answer is, “Yes.” OAS has become all of these things at once. That is why reform is difficult.

Canada has already tried to address the issue of the rising cost of OAS: start the benefit later. The Harper government legislated a gradual increase in the eligibility age from 65 to 67. The Trudeau government reversed that change before it took effect. That history matters because it reminds us that there are several ways to reform OAS. We can change the starting age. We can change the amount. We can change the recovery tax. We can change GIS. Or we can change some combination of these.

The current debate is really several debates tangled together.

If the problem is unequal treatment between ages 65 to 74 and age 75-plus, extending the 10% increase makes sense.

If the problem is senior poverty, strengthening GIS may be more direct.

If the problem is the stress OAS payments place on the federal budget, then the recovery tax, eligibility age, or general revenues come into view.

If the problem is intergenerational fairness, then benefits paid to higher-income retirees become harder to justify.

If the problem is retirement security, then stability and predictability matter.

The concerns and options are numerous.

The options look different once the question is clearer

Direction 1: Expand OAS

This is the Bloc-style approach.

It is simple and understandable. If the 10% increase is justified for those 75 and older, it is not hard to see why those aged 65 to 74 would ask to be included.

But it is expensive and not well-targeted. Some money would go where it is desperately needed. Some would go where it is not.

Direction 2: Target OAS more tightly

This is the Generation Squeeze/Fraser Institute-style approach, though they would not frame it identically.

It asks why higher-income retirees should continue receiving a benefit funded from general revenues. Lowering the recovery-tax threshold or using household income could make OAS more targeted.

But targeting creates its own problems. It can increase effective tax rates, complicate planning, and penalize retirees whose income is temporarily high because of RRIF withdrawals, capital gains, or other one-time events.

Direction 3: Strengthen GIS and the public pension floor

This is closer to a CCPA-style approach.

If the goal is to reduce senior poverty, GIS is more direct than a broad OAS increase. But the language needs to be careful. GIS is tax-free, but it is income-tested. OAS is taxable but does not count for GIS purposes. TFSA withdrawals are not taxable and do not count either. Other income, such as CPP, RRIF withdrawals, workplace pensions, investment income, and employment income above the applicable exemption, can reduce GIS.

Strengthening GIS may be a better way to help seniors with the lowest incomes, but the income-testing formula still matters. A benefit can be tax-free and still be reduced as countable income rises.

Each approach answers a different question. Expanding OAS answers the age-fairness question. Targeting OAS answers the fiscal and income-targeting question. Strengthening GIS answers the poverty question. None of these answers is complete because OAS is being asked to do more than one job.

Reform should begin by naming the purpose

My own view is that OAS should return to its original purpose, to reduce senior poverty.

Arguing for broad benefits may be politically palatable, but it is expensive. Targeted benefits are more efficient but can be complex and sometimes punitive at the margins. Age-based benefits are simple but imprecise. Raising eligibility ages saves money but may be hardest on those least able to adapt. Even my favoured rationale, poverty-focused benefits, while better targeted, may miss people who are not poor but still financially fragile.

For individual retirees and near-retirees, the practical lesson is more modest. OAS remains an important part of retirement income planning, but it is not immune from political debate. Most people should not build a retirement plan around speculation concerning policy changes. Still, it is wise to remember that OAS is not a contributory pension like CPP. It is a government program paid from current federal revenues, and government programs can change.

This is the 310th blog post for Russ Writes, first published on 2026-06-15.

If you would like to discuss this or other posts, connect on Facebook, Twitter aka X, LinkedIn, Instagram, Mastodon, or Bluesky.

If you are an existing client, please contact me by email for an appointment.

If you are a potential new client seeking an advice-only financial planner, I am preparing for retirement and am no longer accepting new clients. Please go to the Advice-Only Planners website. All members listed are also members of the Financial Planning Association of Canada.

Disclaimer: This blog post is intended for general information and discussion purposes only. It should not be relied upon for investment, insurance, tax, or legal decisions.

Image created by ChatGPT