The Hot Potato Portfolio

Norman Rothery’s Heated-Up Version of the Couch Potato Portfolio

The Original Couch Potato Portfolio

The original Couch Potato Portfolio came from a 1991 article by Scott Burns, then a writer at the Dallas Morning News. He advocated for a simple two-fund portfolio using index mutual funds. One would track the S&P 500 stock index, and the other tracked the US total bond index. The portfolio was weighted 50/50 between the two funds.

MoneySense Magazine and the Canadian Couch Potato

According to Dan Bortolotti, formerly a journalist and now a portfolio manager at PWL Capital, when MoneySense magazine was launched in 1999, Ian McCugan, the first editor of the magazine, brought the Couch Potato Portfolio to Canada.

At its simplest, the Canadian version modified the original US version by adding a Canadian equity fund and exchanging the US bond fund for a Canadian bond fund. With three funds, the new weightings were 1/3 Canadian equity, 1/3 US equity, and 1/3 Canadian bond.

Eventually that was diversified into a Global Couch Potato portfolio consisting of four funds: 20% Canadian equity, 20% US equity, 20% International equity, and 40% Canadian bond. With this mix, you get the classic 60/40 portfolio, 60% in equities split equally across three different geographical categories: Canada, the United States, and the markets of developed countries around the world (International), with the remaining 40% balanced by a holding in a Canadian bond fund.

Over the last decade or so, Dan Bortolotti has been the biggest popularizer of this approach. He owns the Canadian Couch Potato website, home to a blog and a series of model portfolios that adjust the weightings and funds depending on your risk tolerance and money available to invest. A beginning investor looking to build an investment portfolio would do very well to start with Bortolotti’s website.

The Hot Potato Portfolio

Another popular writer in the world of finance, and for years a regular contributor to MoneySense and other publications, is Norm Rothery. He is the founder of the Stingy Investor website and publisher of The Rothery Report investment newsletter. Much of his focus is on “value” investing, an active investment style that seeks out stocks that are undervalued relative to their intrinsic worth.

In 2015, Rothery wrote an article introducing a new kind of couch potato portfolio which he referred to as the “Hot Potato” portfolio. With this approach, he suggested combining the essentially passive index funds used in couch potato investing with an active “momentum” strategy.

Momentum Investing

Momentum investing is a strategy that seeks to take advantage of the observation in the market that stocks that do well tend to continue that trend. For example, an investor might decide that technology stocks have done very well over the last several months and decide to invest heavily in that sector. By contrast, energy stocks have done poorly and so the momentum investor would completely avoid investing in that sector.

Rothery’s Hybrid Approach: The Hot Potato

Rothery combined the Couch Potato investing approach with momentum investing to create the hybridized Hot Potato portfolio. This is definitely a more aggressive approach to investing. Instead of setting an asset allocation and sticking with it, the addition of the Momentum strategy means you go “all in” on the asset class that has done well over the previous year. Therefore, if in the last year, US stocks did the best, then you would sell everything else and buy only the US stock index fund. If a month later, you looked back on the year once again and International stocks had done best, then you would sell your US fund and buy the International fund. And if we ran into another month like we had in March 2020, then it is most likely that the best performer would be bonds, in which case you would sell the International fund and buy the Bond index fund.

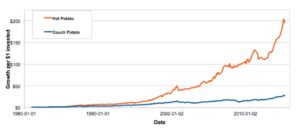

The results, according to his 2015 article, were remarkable:

Hot Potato investors who rebalanced each month into the top performing asset class of the prior 12 months gained an average of 16.6% annually from the start of 1981 to the end of April 2015. They beat the regular Couch Potato by a whopping 6.5 percentage points annually. You can examine the return history of both in the accompanying graph.

Source: https://www.moneysense.ca/columns/the-hybrid-investing-approach-passive-active-portfolio/

There are certainly some caveats to point out with this approach. First, there is the rather standard disclaimer that past performance does not guarantee future results. Second, there are trading costs associated with such an approach that are not reflected in the chart above. If the movement in the markets is quite volatile, you could find yourself making monthly trades. If there are commissions involved, as there often are when trading ETFs, frequent trading will reduce your returns. Bid-Ask spreads are another aspect of trading costs in that you typically get a slightly lower price (the bid price) when you sell, and pay a slightly higher price (the ask price) when you buy. Third, an investor who does this kind of trading in a non-registered account may be subject to capital gains taxes or at the least, somewhat more complex tax-filing. For this reason, it is probably more convenient to confine the Hot Potato Portfolio to tax-free or tax-deferred accounts like TFSAs or RRSPs. Fourth, there is always the possibility that a single category could perform so badly that the portfolio will be irreparably damaged before the switch can be made. Maintaining a balance with fixed income and equities from other categories won’t stop losses altogether but it should reduce the severity of such losses.

An alternative would be to invest in index mutual funds rather than ETFs. These typically do not have trading costs and usually do not charge fees if you hold the position for at least 30 days before selling it again. There would be a slightly higher MER, however. Rothery’s research suggested that, on average, there were only 1.7 large trades per year, so the number of trades may not be that onerous.

Cooling Off the Hot Potato

Some people are risk takers by nature. For such people, concentrating their portfolio in a single category, as the Hot Potato approach does, is not an issue. Others are more cautious and want a simple investing approach that requires little action on their part. For them, a broadly diversified balanced mutual fund or asset-allocation ETF will do the job just fine. However, there may be a few people out there who are intrigued by the Hot Potato idea but want to temper the heat a bit. For those people, these two options may be worth considering:

1. Maintain a Fixed Income (Bond) Component

Let’s suppose that you have assessed your risk tolerances and required rates of return and have decided that a 60% equity / 40% fixed income asset allocation works for you. You could simply maintain your 40% fixed income holding and only adjust the equity portion. In fact, if your fixed income portion is held in a series of GICs, then you cannot trade out of them anyway until they mature. In this scenario, at the beginning of a new month, you would put the 60% equity portion entirely into the best performing of the three equity funds: Canadian, US, or International. And, when a major downturn occurred, and all three of the equity funds performed poorly, you would put everything into a fixed income or bond fund and leave it there until one of the three equity funds became the better performer again.

2. Use Asset-Allocation ETFs

Asset-Allocation ETFs, like those offered by Vanguard, BlackRock’s iShares, Bank of Montreal, and others, are so-called one-ticket solutions. Among the providers, asset allocations can range from as aggressive as 100% equity to as conservative as 20% equity and 80% fixed income. When the stock market is showing a year-long record of trending upward, you would invest in a 100% equity portfolio, but as soon as the 20/80 portfolio began to outperform you would make the switch. Given the year we have had, you may have chosen to switch out of a 100% equity portfolio in late February and then gotten back into it later in the year.

Obviously, there is no perfect solution. In my last blog post, I wrote that I target a 50/50 equity/fixed income portfolio for my investments; taking bigger risks with the investments that I hope will fund what could be several decades in retirement, is not the kind of risk I am interested in at this point. However, for the right kind of person, this may be a helpful approach. Certainly, for the person seeking to hit a home run on a single stock the Hot Potato Portfolio strategy is downright conservative. I will leave it to you to decide if the Hot Potato is at the right temperature for you.

If you would like to discuss this or other posts, connect on Facebook, Twitter or LinkedIn.

Click here to contact me for an appointment.

In these uncertain economic times, you may be interested in a half-hour no-cost, no-obligation financial planning conversation with me. It’s called FINPLAN30 and the range of topics is wide open. Click here to sign up for a free session.

Disclaimer: This blog post is intended for general information and discussion purposes only. It should not be relied upon for investment, insurance, tax, or legal decisions.