The Benefits of Charitable Donations

An Introduction to Tax Planning – Part 5

The numbers of people who are applying for Employment Insurance (EI) and the Canada Emergency Response Benefit (CERB) and other supports that the government has rolled out in recent weeks are just staggering. Perhaps, like me, the figures are beginning to cause your eyes to glaze over and you are barely able to take it in anymore. The financial impact, largely imposed by our governments, is unprecedented, but necessary to save lives.

For those who have been deeply affected, many have turned to charitable organizations for resources. For example, food banks have seen significant increases in demand for their services. There are many in need, but there are also many for whom the financial impact has been bearable, and in some cases, negligible. If you are among those with extra resources, this crisis may be a time to consider how your money can benefit others.

Charitable Giving and Taxation

It may seem odd to write about charitable giving in a series on tax planning. However, our government’s tax system encourages charity by providing some tax benefits for taking that sort of action.

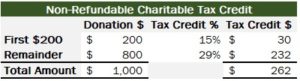

Assuming the charities to which you donate are registered and eligible to provide receipts, you can claim up to 75 percent of your net income, with some exceptions. For most of us, that is probably beyond our means to give that much. At the federal level you receive a tax credit of 15 percent on the first $200 donated, and 29 percent on amounts in excess of $200. Here’s an example of a donation of $1,000 to a charity:

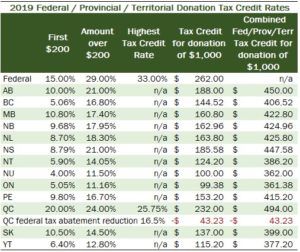

TaxTips.ca is a great site to research information about taxation. The following table, which I have adapted from their site, provides a summary of the donation tax credit rates across the country for 2019.

Beyond the credits themselves, there are some strategies you can use to optimize the tax value of your donations.

Combine Donations Between Spouses

If you are married, you can combine your donations between the two of you. The combined credit should usually be allocated to the spouse with the higher taxable income. Doing so will avoid having both spouses receive the low-rate credit on the first $200 twice. Furthermore, if one spouse is in a high- income tax bracket such that they are charged a surtax by their province of residence, then the impact of the tax credit will provide a moderate tax advantage.

Donating Cash versus In-Kind Donations of Appreciated Securities

With the market crash following the COVID-19 pandemic, the value of many securities will have dropped. Nevertheless, you may have stocks or equity funds that are still up a great deal. The following table, originally from Abundance Canada, provides an example of donating securities to charity.

You can see that by donating securities directly rather than liquidating them to generate cash, you can save significant amounts in capital gains tax and still get the full value of your donation. You should note that the concern for capital gains tax implies that the donation is made from a non-registered account.

Combine Two or More Years of Charitable Donations Into One Year

Sometimes income may be low in a certain year making it difficult to give as much as you would like. If you are donating small amounts in the course of a year, you can choose not to recognize the donation in your current year. Instead, you can carry the donation forward to claim on your return for any of the next five years along with any other donations you have made but not yet claimed during that period. This will potentially give you access to the higher tax credit rate of 29 percent.

How to Give

Donating Directly to the Charity

I am not expecting any door-to-door canvassers for donations coming around in these self-isolating days, so donations of cash straight out of your wallet are an unlikely occurrence. I will admit that I am not much in favour of this sort of thing anyway, because I think donations are more effective when they are planned, and you really know the charity to which you are donating. Rather than door-to-door, the better choice, often with easier processing for both the donor and the charity, is to donate online. Of course, mailing a cheque and sending it to the charity is also an option.

Donating via a Donor-Advised Foundation or Fund

Earlier I noted the potential benefit of donating appreciated securities from your non-registered account. Not all charities are set up to receive other than cash (cheque or credit card) donations, however, so a way around that is to donate your securities via a donor-advised foundation. Abundance Canada, which I mentioned above, is one such foundation. You can transfer in-kind donations to a donor-advised foundation and they will distribute the funds to the charity(-ies) of your choice.

There are at least two benefits to this path.

Benefit 1: You only have to deal with one receipt

You only have to donate to one entity, the foundation, and receive a single receipt from the foundation. You then simply provide your instructions and the foundation takes care of the rest.

Benefit 2: You can maintain anonymity

By donating through a foundation, you have the option of making your donation to a charity anonymously. While many of us appreciate the opportunity to be generous to a charity that does good in our world, we may find that, once you are on the charity’s mailing list, you begin to receive repeated requests for additional donations. By donating anonymously, this issue is avoided.

Some Giving Suggestions for These COVID-19 Days

While doing research for this post, I came across a charity by the name of Charity Intelligence. They research Canadian charities so that potential donors can be informed and give intelligently. They have free reports on more than 750 Canadian charities. Through their site I have a few suggestions for you if you are thinking about donating but are not sure about your next step.

International Charities

Canada is absolutely challenged by COVID-19 but at least we have the healthcare infrastructure to address this pandemic, even if we often feel it is not adequate. That is not often the case in the developing world, and, as the word pandemic implies, this disease is going to spread everywhere. For that reason, Charity Intelligence recommends the following two agencies:

Doctors Without Borders (Medicins Sans Frontieres) is a remarkable medical humanitarian charity, delivering medical care in response to conflicts, natural disasters and other emergencies. You can donate here.

Farm Radio International’s communication platform of radio programs, over 1,000 stations across 41 African countries, helps spread critical information to people about COVID-19. We all know how much we are depending on information for ourselves these days. It makes just as much sense elsewhere. You can donate here.

Local Charities

With many people losing part or all of their employment, and with the inevitable delay before the many measures taken by our governments in Canada come into full effect, food banks have found that demand for their services has increased even more. Charity Intelligence Canada has published a list of food banks in Canada here. I will note that one of the food banks listed, Canadian Foodgrains Bank, actually supports food security around the world, so they could also easily fit under charities that work in international contexts.

Resources

Charity Intelligence

In addition to what I wrote above, you can find more information about Charity Intelligence here.

Abundance Canada

Abundance Canada is a donor-advised foundation that I have been familiar with for many years. Personally, my family and I use it as a path for most of our charitable giving. Even if you choose to give by a different path, their website, accessible here, can provide you with a great deal of helpful information about charitable giving.

If you happen to be in the business of providing financial advice, Abundance Canada also has a section for professional advisors, which you may find useful.

Next Time

In my next post I will begin a series on Retirement Planning.

If you would like to discuss this or other posts, connect on Facebook, Twitter or LinkedIn.

Click here to contact me for an appointment.

In these uncertain economic times, you may be interested in a half-hour no-cost, no-obligation financial planning conversation with me. It’s called FINPLAN30 and the range of topics is wide open. Click here to sign up for a free session.

Disclaimer: This blog post is intended for general information and discussion purposes only. It should not be relied upon for investment, insurance, accounting or legal decisions.

Image by Capri23auto from Pixabay