Lump-Sum Investing vs. Dollar-Cost Averaging

The Situation

A relative of yours has died. You have received an inheritance. With that money, you have paid off your mortgage and your car loan. You have topped up your Registered Retirement Savings Plan (RRSP) and you have set aside six months of living expenses in an emergency fund. Until now you have never had enough extra money to contribute to your Tax-Free Savings Account. Now you have $60,000 of your inheritance remaining and with no particular place to spend it, you decide it needs to go into a TFSA. You are a bit anxious about investing all that money at once and wonder whether it makes more sense to put in a little at a time. What should you do? Let’s consider the options.

The Options

Lump-Sum Investing

Positive

It makes logical sense to invest your entire inheritance in a lump sum. The investment markets over the long term have historically been on an upward trend. Why spread out your investment over time when the odds are that it is likely to become more expensive each time you invest?

Negative

Periodically investments have gone down. If you were born in the mid 1980s or earlier, you have seen dramatic drops in the value of investments in 2000 – 2002, 2007 – 2009, and perhaps most dramatically, earlier this year. Logic doesn’t do much for you when you’re wondering whether that money you had invested will even be there when you retire.

Dollar-Cost Averaging (DCA)

Positive

Markets can be, and often are, volatile. They go up and down and they can make you emotionally sick. DCA is like medicine to your psychological soul. If a downward trend persists, which can happen, using a DCA approach can help maintain your calm when markets are roiling and allow you to keep investing.

This is really where DCA shines. If the markets have declined in value and they continue in a generally negative trend for the next year, your choice to invest a portion of your inheritance each month for 12 months will be much more beneficial to you than if you had invested it all in a lump sum before the market slump.

Negative

Both history and theory argue that, most of the time, DCA does not work. Vanguard, the US investment giant, studied these alternatives and showed that about two-thirds of the time it is better to invest in a lump sum.

Another negative factor is that your asset allocation is temporarily altered. If you had decided that your accounts should be invested in a mixture of 60 percent equities (stocks) and 40 percent fixed income (bonds and GICs, etc.), leaving most of your investment in cash or cash-like investments like a money market fund or an investment savings account means that your portfolio is overly skewed toward the conservative end of the investment spectrum, potentially hurting your long-term returns.

The Analysis

For the purposes of this analysis, I am going to look at the one-year return of the Vanguard Growth ETF Portfolio, VGRO. Eighty percent of the fund is invested in equities (stocks) and twenty percent is invested in fixed income (bonds). For someone with a long time horizon, this may be a suitable investment allocation. I will further assume that no commissions are paid to purchase the ETF and that dividends will be reinvested in whole shares, with the balance left in cash. Which approach makes more sense?

Investing a Lump Sum

The table above shows an initial lump sum of $60,000 invested at $25.60 per unit (or share), resulting in an initial position of 2,343 units with $19.20 remaining. After that, the only new cash into the account were four distribution payments that were reinvested into additional units of VGRO at a price available on that particular day. The final column shows the value of the account as of the closing price on July 13, 2020. The lump sum approach yielded an effective one-year return of 4.72%.

Here is a simple line chart of how the balance changed over the period measured in the table, to give you more of a visual representation:

Investing by Dollar Cost-Averaging (DCA)

The table above shows an initial purchase of $5,000 and then subsequent monthly purchases of $5,000 on or around the 15th of each month until the entire $60,000 has been fully invested. As before, distributions are also fully reinvested. The final column shows the value of the account as of the closing price on July 13, 2020. The DCA approach yielded an effective one-year return of 4.83%, 11 basis points (0.11%) higher than the lump-sum approach.

The chart immediately below gives a better visual representation of how the account balance changed over time:

In addition to the feeling that by purchasing a smaller amount over an extended period of time, you are reducing the risk of loss, this chart also provides another reason why investors might find this approach appealing. For the most part, the chart keeps on going up. Yes, there is a small dip, which represents a drop in the unit price of VGRO at the time of the March 16, 2020 purchase, but I think that most people would feel quite satisfied by this chart, compared to the ups and downs in the lump-sum investing chart.

A Hybrid Approach

As noted earlier, about two-thirds of the time, a better outcome will occur when investing a lump sum versus dollar-cost averaging. In our particular one-year example, it actually worked out in favour of DCA, thanks to the volatility we have been experiencing in 2020 so far. With those statistics in mind, I wondered whether the ideal way to manage the risk of a downturn in the markets would be to invest two-thirds of the lump sum at the beginning of the period while using dollar-cost averaging to invest the remaining one-third. Using the same $60,000, I took $40,002 (necessary to avoid rounding) and invested it in a lump sum on July 15, 2019, and divided the balance of $19,998 into 11 monthly investments of $1,818 each. As you can imagine, the result came in between the two “pure” approaches, at 4.76%.

How would you feel about the chart? It starts off at a higher level but the drop in in mid-March 2020 is much more pronounced. Even so, this approach is better than the lump-sum approach in this particular situation, while performing slightly worse than the DCA approach.

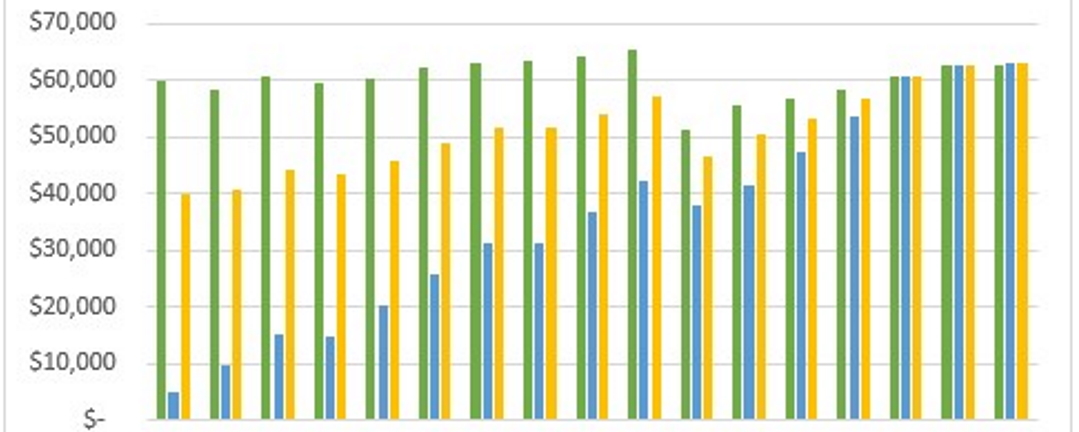

The Three Approaches Compared

As the above table makes plain, despite the different approaches, all three wound up with pretty well close to identical outcomes. A different data set would no doubt produce a different result. Nevertheless, I find it fascinating that the three approaches could be so close as to appear virtually identical.

Practically Speaking

The reality is that, while many of us may get an inheritance, the opportunity to engage in Lump-Sum investing is probably not going to come our way very often, even if it is most likely going to produce the better outcome. Aside from the rare circumstance of an inheritance, most of us will dollar-cost average our way toward wealth for no other reason than we only get paid periodically.

If you would like to discuss this or other posts, connect on Facebook, Twitter or LinkedIn.

Click here to contact me for an appointment.

In these uncertain economic times, you may be interested in a half-hour no-cost, no-obligation financial planning conversation with me. It’s called FINPLAN30 and the range of topics is wide open. Click here to sign up for a free session.

Disclaimer: This blog post is intended for general information and discussion purposes only. It should not be relied upon for investment, insurance, accounting or legal decisions.