In Praise of Mutual Funds

Mutual funds do not get a lot of love, even though they hold the lion’s share of retail investors’ assets in Canada. If you are like me and often peruse personal finance pages of the major Canadian newspapers (or more accurately, their websites), you will often find advice in the comments following any given article that the first thing an investor should avoid is mutual funds. The recommended alternative is typically: 1) Invest in ETFs (Exchange-Traded Funds); or, 2) Invest in dividend stocks.

I have some problems with these assertions:

- Mutual funds are widely varied in Canada, with over 4,000 to choose from. In the TMX group of companies, which includes the Montreal Exchange, the Toronto Stock Exchange, the TSX Venture Exchange, and the TSX Alpha Exchange, there are only about 3,400 different stock listings, so there are more funds than there are listings.

- Exchange-Traded Funds, while generally considerably less expensive in terms of their management expenses, are less convenient for the average investor. The increasingly wide and varied choice in the ETF world also makes choosing the right product no less challenging than choosing from the available mutual funds.

- The purchase of individual stocks, whether focussed on dividends or some other characteristic, can be a daunting challenge as well. Mutual funds and ETFs usually give an investor a fighting chance at eliminating the idiosyncratic risks of particular securities; individual stock selection invites risks that are difficult to eliminate unless you have a large sum of money available.

Praiseworthy Characteristics of Mutual Funds

Ease of Purchase

In my estimation, one of the biggest characteristics in favour of mutual funds is their relative ease to purchase over ETFs or stocks. Securities that trade on an exchange have a bid price and an ask price and you must make your purchase by determining the number of shares or units you can buy (or sell) at a given price.

Imagine it is noon in the eastern time zone. You have $5,000 to buy an ETF. The price at which the ETF has traded since the market opened at 9:30 that morning has fluctuated from $24.96 to $26.21. The last trade was at $25.19. For this case, let’s assume there is a $9.99 commission. You want to use all $5,000 to buy the ETF. First, you have to subtract the commission. $5,000 – $9.99 = $4,990.01. Since you are buying you have to figure out what price you are prepared to pay per unit. The last trade was at $25.19 but the current bid and ask is $25.20 and $25.23. As a buyer, to be confident of getting your order filled, you have to match the ask price of $25.23. You divide that number into the cash available: $4,990.01 ÷ $25.23 = 197.78. However, you can only buy whole units, so you need to round down your purchase to 197 units (or shares). 197 x 25.23 = $4,970.31 + $9.99 = $4,980.30, which means you have left $19.70 uninvested.

Contrast that situation with a mutual fund purchase. You go to the order entry page, select the mutual fund you want to purchase, punch in the dollar amount, and you will be able to buy units of your mutual fund down to the last penny, with nothing left over.

No Intra-Day Trading

ETFs and stocks trade throughout the day, typically Monday to Friday, from 9:30 am to 4:00 pm ET. Yes, you can put an order in outside of the market hours, but if you set a price indicating how much per unit you are willing to pay, your order might not get filled at all. Imagine that in the scenario above, the ETF described above had closed at $24.89 at the end of the previous trading day. You decided to put in an order to buy, good for the next day, at $24.93. However, the ETF never got lower than $24.96, so your order never got filled.

You don’t have to specify a price, as in the above scenario. That is referred to as a limit order. Instead, you can take whatever the market is offering, which is a market order. That can work out okay, but it is also a potentially dangerous situation. What if there is really good news about that ETF, or the securities underlying that ETF, after you put in your market order and the ETF’s price per unit shoots up to $27.42 as the market opens. At the time you had put in your market order to buy 200 units you had estimated that the price of the ETF would not rise above $24.95 that morning. Well, you bought your 200 units, but at $27.42 and with the $9.99 commission, you would have paid a total of $5,493.99, almost $500 more than you intended. If you can cover the balance owing in two business days, it isn’t such a big problem, except that you paid more than you expected, but if you are unable to pay the amount owed, you might have to sell it. That can cause problems in two ways. First, regulations require that you need to pay for a position – or provide sufficient collateral in the case of a margin account – before you sell it. Failure to do so will result in a violation that could restrict your ability to enter orders. Second, you may have bought the ETF at $27.42, but there is no guarantee that you will be able to sell it at that price. You could lose money.

Price Equals Net Asset Value

Contrast that with a mutual fund purchase. You specify a dollar amount, and your order is filled at the closing “Net Asset Value Per Unit” as of that day. It’s simple and straightforward.

Diversification

In this respect, ETFs and mutual funds are not that different. With a single purchase of an ETF, you can invest in a broad range of assets, often representing a proportionate weighting of an entire stock market or bond market index. This approach of simply replicating an index means that there are no efforts to create a customized portfolio of individual securities designed to outperform a certain “benchmark” index. In recent years, new customized rules-based indices have been created and such ETFs are much more like actively managed mutual funds.

Mutual funds, although they have a reputation for being exclusively actively managed products, also include within their range of products several funds that only seek to replicate broad-based indices. Nevertheless, it is certainly the case that more mutual funds are actively managed, which brings with it necessarily higher costs for the research required to make the appropriate purchases for the fund. Also, instead of potentially having 100s of stocks in an index-tracking ETF, an actively managed mutual fund may hold only 20 to 50 stocks. Even so, this is generally a risk-reduction strategy in that the selection is more diversified than buying a selection of individual stocks representing companies all in the same industry. In Canada, that might mean the big bank stocks, natural resources stocks, or more recently, cannabis stocks.

Commission Differences

Here I am referring to a fee charged by your financial institution to buy or sell a fund. Some brokerage firms allow you to buy ETFs without commission, but you have to pay a commission when you sell. Other firms will have a smaller list of commission-free ETFs. I believe there are only one or two firms or platforms that allow you to both buy and sell ETFs commission-free.

In years gone by, many mutual fund firms charged either front-load or back-end-load (a.k.a. Deferred Sales Charge) mutual funds. That fee would go toward the compensation that the mutual fund sales representative would receive for having sold the fund. The sales representative would also get a trailing commission that would be paid from the management expenses of the fund by the fund company as long as you continued to own the fund. These days, such so-called load funds are disappearing. Instead, if you are working with an investment advisor, you might get what is called an F-series fund in which the fund’s management fee is stripped of the trailing commission. Instead, the advisor charges you a fee directly.

Several mutual fund companies do not pay trailing commissions at all. Instead, they sell directly to the investing public, typically for a much lower fee than you would pay when going through an advisor. Having said that, you are limited to that particular company’s mutual funds.

In the discount brokerage world, where no specific investment advice is provided, in addition to some of the funds from the lower-priced direct selling companies, you can find mutual funds from a variety of the well-known mutual fund companies, including those from the big banks, but they are the so-called D-series funds (think D for Discount), for which the advice portion of the management expense ratio has been removed.

Automatic and Full Reinvestment of Distributions (Dividends)

If you invest through a discount broker, you can typically enrol your account, or even specific ETFs (or stocks) in DRIP, a Dividend Re-Investment Program. Because many stocks pay out dividends periodically, so do the ETFs that hold those underlying stocks. Some pay monthly, others quarterly, still others semi-annually or even annually. You can choose to enrol those positions in DRIP so that instead of getting paid to you in cash, the dividend or distribution can be reinvested in the underlying ETF. No commission is charged for this service.

To illustrate, let’s imagine you held 100 shares of an ETF with a price of $25 per unit. The ETF paid $0.75 per unit over a year, evenly split into four quarterly distributions, which works out to $0.1875 per quarter per unit. At the current price of $25, that works out to a 3% distribution. Each quarter you would receive $18.75. Unfortunately, $18.75 is not enough to purchase even one unit as it is less than $25 and in the world of ETFs bought at discount brokerages in Canada, you can only “DRIP” whole units, not fractions.

One solution is to hold more of the ETF so that your distributions make up at least one unit. If you owned 134 units, all else being equal you would generate a distribution of $25.13 each quarter, which would be enough to buy 1 unit. Of course, the price of your ETF might increase – which is a good thing! – leading to your distribution once again being too small to purchase another unit.

This is not an issue with mutual funds, fortunately, as they easily handle fractional amounts and will reinvest your distributions in full and automatically.

Possibility of Systematic Investment Plans

Brokerage firms will allow you to set up a pre-authorized contribution to your investment accounts. What they generally cannot do, however, is set up a pre-authorized Systematic Investment Plan (SIP) for ETF purchases.

Let’s imagine that you had set up a pre-authorized contribution to your TFSA of $500 per month. You want to buy shares of a particular ETF each time the deposit hits the account. On the positive side, your account is at a firm that does not charge a commission to purchase ETFs. However, you have to log into your account and enter an order to make the purchase. Furthermore, given the limited dollar amount, you will probably want to put in limit orders while the market is open so that your orders can get filled.

Contrast this with mutual funds. Not only can you set up a pre-authorized contribution, but you can also set up a SIP in which the dollar amount specified goes into the mutual fund, or funds, down to the penny. There is no need for you to intervene.

From a behavioural point of view, the option of a SIP is much superior, in my opinion. With a little bit of paperwork, a phone call, or an online selection, you can basically “set it and forget it” when it comes to mutual fund investing. It all happens automatically.

Imagine that the market is up dramatically. If you have to make your purchase manually, as you must with an ETF, you might look at the price and decide it is too high. You could easily say to yourself, “I’ll wait until next month’s contribution – maybe the markets will have calmed down a bit and I can get a better price then.” The opposite scenario could also present itself: the markets are tumbling down; instead of buying $500 more into that ETF, you are wondering whether you should sell out of it entirely and stay in cash until the markets start turning positive again.

While your anxieties about the markets may not disappear entirely if you use mutual funds and a SIP, because everything is happening automatically you may not even look at your account that often since there is nothing that you need to do. The psychological advantage of this approach should not be underestimated. We investors tend to shoot ourselves in the foot or otherwise mess up a good investment plan by intervening too frequently. Setting up an investment plan and sticking with it over the long term by automating your procedures will almost certainly serve you better.

Final Thoughts

Fees

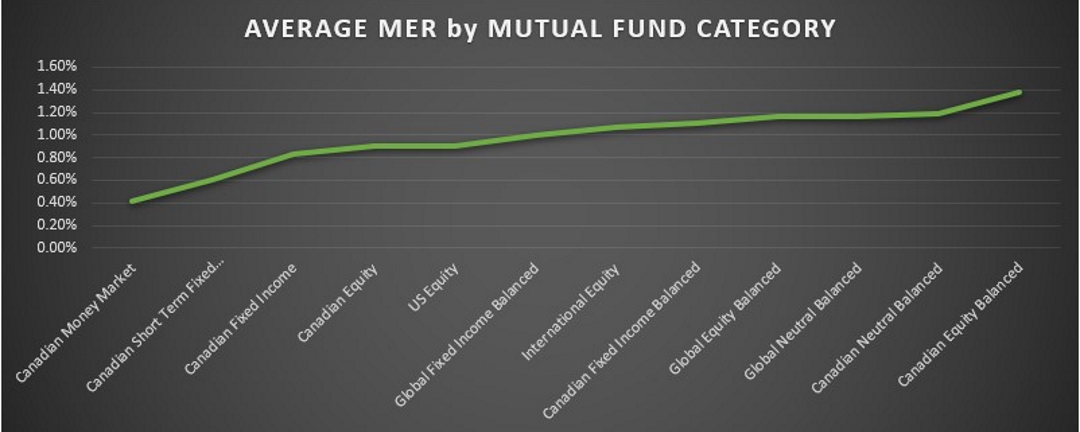

One of the big advantages that most ETFs have over mutual funds is the substantially lower management expenses charged by the former. Repeated studies by research firms such as Morningstar, as well as others, show that fees are the most reliable indicator of investment returns. I don’t know whether I can offer a threshold Management Expense Ratio (MER) at which a mutual fund should be disqualified from consideration, but if you are considering the purchase of a mutual fund, comparing fees is worth your effort.

Asset Allocation

From my earliest studies of investing, it has been pointed out to me that the mix of your assets is a key determinant of your investment returns. If you put all you have into GICs, you know that you are probably going to return less than 2% per year over the next few years. If you leave it in a savings account, depending on the financial institution, you could be getting less than 0.5% in interest. If you put your entire investment portfolio in stocks, you may get 7% or greater in certain years, from a combination of dividends and growth, but periodically, you could also experience a loss of 20% or more. Mixing your assets among cash, GICs, bonds, and stocks from all over the world, and in proportions that make sense to you at your time of life and in line with your willingness to tolerate fluctuations in the value of your accounts, is one of the most important investment decisions you – or your investment advisor – can make.

Behaviour

Finally, I want to reiterate the importance of controlling your behaviour. The difference between the returns of the market versus the returns of the average investor is striking. A report from 2017 showed that over 30 years, U.S.-based equity investors earned about 4% per year, while the benchmark equity index in the U.S., the S&P 500, returned over 10%. While some of this difference can be explained in fees, the short-term focus resulting in trading in and out of the market at the wrong times is the cause of most of this difference. People may complain that the market is rigged against them when the reality is that our brains are rigged against us. Often, the best way to deal with our traitorous minds is to set our investments on autopilot and leave it alone. Mutual funds are a great way to make that happen.

If you would like to discuss this or other posts, connect on Facebook, Twitter or LinkedIn.

Click here to contact me for an appointment.

In uncertain economic times, you may be interested in a half-hour no-cost, no-obligation financial planning conversation with me. It’s called FINPLAN30 and the range of topics is wide open. Click here to sign up for a free session.

Disclaimer: This blog post is intended for general information and discussion purposes only. It should not be relied upon for investment, insurance, tax, or legal decisions.

Feature Image Data Source: TD Direct Investing Webbroker