I’m not old; you’re just young! Retiring when there is an age gap between spouses

An Introduction to Financial Planning – Part 3

A question was put to me via Twitter in response to my last post on retirement planning. In a nutshell, how do couples do retirement planning when there is an age gap between spouses? I will interpret an age gap as equal to 10 years or greater. Typically, though not always, in the case of heterosexual couples the older spouse is male.

When Should We Retire?

Let’s assume a 10-year age gap. Does the couple want to retire together? If we assume a retirement age between 60 and 70 for the older spouse, then the younger spouse is going to retire somewhere between ages 50 and 60. This is both a financial question and a personal/lifestyle question.

Financial Considerations

On the financial side, the younger you retire, the more that is needed to fund a correspondingly longer retirement period. How long will that retirement period be? FP Canada provides Projection Assumption Guidelines including a Probability of Survival Table. Between the ages of 50 and 60, there is a 25 percent chance that one of the spouses will live to age 98. From the perspective of the retiring 50-year-old, that means 48 years in retirement. If the couple delays retirement until the older spouse is 70 and the younger spouse is 60, then there are only 38 years in retirement that need to be funded. One can assume that the older spouse will die about a decade sooner than the younger spouse. If that holds true, then retirement for both only needs to be funded for 28 years, followed by 10 years in retirement as a single person. That does not mean that retirement expenses are suddenly cut in half. A rule of thumb is that a single person has about 70 percent of the expenses of a couple. On the other hand, if long-term care is needed for the surviving spouse, it can be every bit as expensive as before.

Personal/Lifestyle Considerations

On to the personal/lifestyle question. The articles about retirement living often show healthy-looking senior couples enjoying their freedom from schedules by travelling to beautiful locations. If this is an anticipated component of retirement for you, then you may want to retire early to enjoy those activities while you can. In 1998, Michael Stein wrote The Prosperous Retirement. He popularized the three stages of retirement known as the Go-Go Years, the Go-Slow Years, and the No-Go Years. The first stage, the Go-Go Years, is the period of active retirement, lasting until approximately age 75. If the older spouse does not retire until age 70, then fewer years are available for world travel or whatever new passions you wish to cultivate. Of course, this involves some calculation. Can you retire earlier and still have enough for your Go-Slow and No-Go Years?

Another more personal question has to do with employment? Do you enjoy your work? Are you physically able to still do the job? People are living longer healthier lives on average, but you can probably imagine an older spouse working in a physically demanding job who just cannot do it any longer. On the other hand, one or both of the spouses may enjoy their jobs, feel a sense of purpose, and appreciate the camaraderie among colleagues.

Perhaps the best answer is to simply agree that each spouse should retire when it makes sense for them personally. That may or may not be the traditional age of 65. Staggered retirement dates can be financially beneficial for couples with significant age gaps. Many who are employed receive supplemental health and dental benefits that disappear at retirement. If the younger spouse continues to work, those lost benefits can continue under the younger spouse’s plan.

When Should We Start CPP/OAS?

I suspect people often think that retirement coincides with the start of Canada Pension Plan (CPP) and Old Age Security (OAS). That is commonly the case, but it does not have to be that way. You are eligible to take CPP as early as age 60 or as late as age 70. OAS is not available before age 65, but it, too, can be delayed until age 70. Why?

Canada Pension Plan (CPP)

For every month before 65 that you begin to receive your CPP your benefits are reduced by 0.6%. Conversely, for every month after 65 that you begin to receive CPP, benefits increase by 0.7%. Let’s assume for simplicity’s sake that at age 65 you are due to receive $1,000 per month in CPP. If you begin your CPP at age 60, that 0.6% per month reduction adds up to a 36% reduction in your CPP. So, instead of $1,000 per month, you are only getting $640 per month. Inflation adjustments will still take place, but you start at this lower base, which continues for the rest of your life. What about at the other end? If you delay taking CPP until age 70 that 0.7% monthly increase works out to a 42% increase, or a monthly CPP of $1,420 per month.

Survivor’s Pension

Given the 25 percent likelihood of both spouses living into their nineties, it seems to make sense to delay CPP as long as possible so as to get the maximum benefit. However, a recent article in MoneySense by Jonathan Chevreau suggests that one might want to reconsider that timing. The issue boils down to the fact that once one spouse dies, “the most that can be paid to a person who is eligible for the retirement pension and the survivor’s pension is the maximum retirement pension.” In other words, if both spouses are already receiving the maximum CPP, the surviving spouse cannot receive a full survivor’s pension in addition to the full regular retirement pension that she is already receiving. That extra CPP money is gone. The difficulty, though, is in deciding in the face of uncertainty, because none of us knows when we will die.

This may suggest, then, that with a 10-year age gap, seeking to maximize CPP by delaying receipt may not be in your best interests, since you may find that much of the older spouse’s pension will not be available for transfer to the surviving spouse after death.

Old Age Security (OAS)

If you reach age 65 and you have been a resident of Canada for at least 40 years after turning 18, you are eligible for a full OAS pension. Currently that figure is $613.53 per month or $7,362.36 annually. As mentioned above, you can delay receipt of OAS to increase the benefit, but the monthly increment is only 0.6% per month after 65 until age 70. There is no survivor benefit like there is with CPP, so once one spouse dies, the amount coming from OAS is cut in half.

For both CPP and OAS, factors to consider include: expected remaining lifespan, employment status and income needs.

Which Age Do We Use for RRIF Payments?

In the year in which you turn 71 you must convert your Registered Retirement Savings Plan (RRSP) or Locked-In Retirement Account (LIRA) into a Registered Retirement Income Fund (RRIF) or Life Income Fund (LIF). Different jurisdictions may use slightly different terms, but the term locked-in generally refers to funds that were received from a Registered Pension Plan (RPP). Unlike in the case of an RRSP, which is funded by personal (or spousal) contributions, you cannot contribute to a locked-in account. Furthermore, once converted to a LIF, there is both an annual minimum payment and an annual maximum. A RRIF does not have a maximum, although there is a minimum payment.

With respect to a significant age difference, one of the most important things to remember is that the calculation of the Annual Minimum Payment (AMP) is determined by the end of year closing value of the account and your age as of the end of the year. Furthermore, regulations allow the older spouse the right, at the time of the RRIF/LIF account opening, to elect to use the younger spouse’s age when calculating the AMP, resulting in lower minimum payments.

The reason one might wish to make such an arrangement is to avoid withdrawing more than necessary. A commonly heard complaint among retirees is that they do not need to withdraw even the AMP because they have other income sources. In the face of the COVID-19 pandemic, the government reduced the AMP by 20 percent of its normal factor for 2020. This was done in part in consideration of the uncertainty and volatility of investments this year.

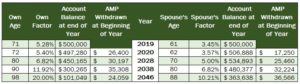

Here is a chart laying out the AMP for a man who turned 71 in 2019. His wife is 10 years younger, so he can use the age of 61 for calculating the AMP. I am assuming a $500,000 account balance at the end of 2019. I also include figures for the 25%-reduced factor brought on because of the COVID-19 pandemic for interest’s sake.

You can see that there is a considerable reduction in the amount that must be withdrawn from the account. The very reasonable goal here is to address the concern that little of the older spouse’s assets will be left to support the younger spouse after the older spouses has died.

The table above excerpts a few years to show the impact of using the younger spouse’s age in determining the AMP. To explain briefly, in 2019 the older spouse had turned 71 and the younger spouse had turned 61. The older spouse was required to convert his RRSP into a RRIF. The end of year value in 2019 was $500,000. Based on the older spouse’s 5.28% factor, he was required to withdraw a minimum of $26,400, which was withdrawn in a lump sum at the beginning of 2020. I assume a 5 percent return on the balance for the remainder of 2020. This causes a smallish decline of $2,720 in the value of the account. In the rows below you can see the factors getting larger, reaching 20 percent at age 95 and older, until the older spouse died in the year he turned 98, with a little over $100,000 remaining in the account.

In the right half, however, in which the older spouse uses the younger spouse’s age to determine the AMP, you can see that the account actually increases in value for the first few years and this time, when the older spouse dies, there is well over $300,000 remaining, which the younger spouse will inherit.

I should clarify that nothing prevents the older spouse from drawing down his RRIF more quickly if necessary. However, it does give more flexibility to spend less in order to preserve more of the RRIF for the surviving spouse’s needs as she manages on her own.

Which is the Better Option for My Defined Benefit Pension?

Defined Benefit Registered Pension Plans are becoming a rarer item these days, but they are still available from some employers. Often, the retiring employee, the older spouse in this scenario, has the choice to take a lesser amount now in order to allow for a relatively larger pension for the younger surviving spouse after his death. For example, a Defined Benefit plan provides for three options:

- Highest level to original recipient, 50% to surviving spouse;

- Mid-level to original recipient, 60% to surviving spouse; or

- Lowest level to original recipient; 100% to surviving spouse.

Similar arrangements can apply if you choose to purchase a joint and survivor annuity with a portion of your Defined Contribution Pension Plan or RRSP. In the situation of a much younger spouse, this option can result in a significant benefit without a large decrease in the amount that is received directly by the older spouse.

Next Time

For my next post on retirement planning I will discuss clarifying your vision for retirement.

If you would like to discuss this or other posts, connect on Facebook, Twitter or LinkedIn.

Click here to contact me for an appointment.

In these uncertain economic times, you may be interested in a half-hour no-cost, no-obligation financial planning conversation with me. It’s called FINPLAN30 and the range of topics is wide open. Click here to sign up for a free session.

Disclaimer: This blog post is intended for general information and discussion purposes only. It should not be relied upon for investment, insurance, accounting or legal decisions.

Image by Arek Socha from Pixabay